In recent years, the Cooperatives Development Authority (CDA) ranked the top cooperatives in the Philippines. They based the ranking mostly on asset size, as this is the most tangible proof that shows the cooperatives’ financial strength, stability, and ability to serve members. After all, knowing which co-ops hold the largest assets means learning about how well they manage funds, expand services, and return benefits like dividends, loans, and community programs. By checking out these top cooperatives—their features, membership requirements, and offerings—we can make smarter choices about where to invest, save, or join for long-term financial and social growth.

In this guide, we summarized everything you need to know about these top co-ops so it will be easier for you to decide, in case you ever need to find a place to invest your hard-earned money.

Types of Cooperatives

The cooperatives that made it to the top of the CDA’s rank list actually did not come from a single type or category. In fact, they can be categorized into different types as follows:

- Military and Uniformed Personnel Co-ops: Co-ops originally formed by soldiers, police, and uniformed services to support financial stability, loans, and family welfare.

- Employee/Institution-Based Co-ops: Workplace-based co-ops giving employees access to savings, loans, dividends, and exclusive perks.

- Community-Based Multipurpose Co-ops: Open to the public, these co-ops provide financial services, social programs, and livelihood support to local communities.

- Agriculture-Based Co-ops: Focused on farmers and agri-business, offering loans, inputs, marketing, and support for rural livelihoods.

- Cooperative Banks: Co-op owned banks serving farmers, small businesses, and communities with savings, loans, and banking services.

- Utility and Service Co-ops: Co-ops providing essential utilities like electricity and communication, with profits and benefits shared with members.

Now that you know that there are different types and purpose to the cooperatives in the top list, let’s take a closer look at the actual cooperatives and what they are made of for better understanding:

1. ACDI Multipurpose Cooperative

ACDI Multipurpose Cooperative started in 1981 as a small group of Air Force members who pooled resources to support fellow soldiers and their families. Today, it has grown into one of the biggest and richest cooperatives in the Philippines, with more than ₱54 billion in assets and over 140 branches nationwide. It provides financial services, business ventures, and community programs that promote financial security and sustainable growth for both uniformed personnel and civilians.

Target Members:

- Active, retired, and reservist AFP members

- Personnel from PCG, BFP, PNP, BJMP, BuCor, and CAAP

- Civilian employees of AFP and ACDI

- Dependents and beneficiaries of qualified members

- Selected employees in the aviation sector

Membership types:

- Regular Member: full rights, including voting and dividends

- Associate Member: limited rights, no voting power

Features and Benefits:

- Savings and deposit products (regular savings, time deposit, Fortune Plan)

- Loans (consumption, livelihood, education, housing, vehicle, and more)

- High dividends and patronage refunds

- Loan insurance and cash assistance for beneficiaries

- Health benefits, training, and seminars

- Business ventures: aviation schools, air charter, ticketing and travel, construction, real estate, agriculture, retail stores, insurance, memorial plans, and security services

2. Philippine Army Finance Center Producers Integrated Cooperative (PAFCPIC)

PAFCPIC, also known as PAPSI, is one of the biggest cooperatives in the Philippines serving soldiers, veterans, and their families. Established in 2009, it provides savings, loans, insurance, scholarships, and other financial programs tailored for members of the Armed Forces of the Philippines (AFP). With over 189,000 members, it has grown nationwide with offices across Luzon, Visayas, and Mindanao.

Target Members:

- Active and retired personnel of the Philippine Army, Navy, and Air Force

- Civilian employees of AFP and PAFCPIC

- Dependents of regular/associate members

- Pensioners from AFP or PVAO

- Other uniformed personnel from government agencies

Membership types:

- Regular Member: full voting rights; includes active Army personnel, civilian employees, retirees, and family of deceased regular members

- Associate Member: limited rights; includes Navy/Air Force personnel, dependents, pensioners, and others under AFP-linked groups

- Sponsored Dependent: parents, spouse, or adult children of a member

Features and Benefits:

- Loans: salary, multipurpose, car, housing, business, calamity, appliance, education, and more

- Savings & Investments: Regular Savings (4.5%), Special Savings (6%), Share Capital with annual dividends (up to 21%)

- Insurance: “We Care” life insurance for only ₱50/month with ₱100,000 coverage

- Member Benefits: free lifetime membership, low loan amortization, patronage refunds (3x yearly), medical aid, scholarships, and sponsorships

- Other Services: leasing of commercial spaces, social and civic programs for AFP units, and corporate sponsorships

3. First Community Cooperative (FICCO)

FICCO is one of the biggest multipurpose cooperatives in the Philippines, starting in 1954 with only ₱26.30 as capital from a small group in Cagayan de Oro. Today, it has grown into a nationwide institution with over 408,000 members and more than 100 branches. It offers savings, loans, insurance, and other services under the principle “Not for Profit, Not for Charity, but for Service.”

Target Members:

- Any Filipino, including OFWs and local residents

Membership types:

- Regular Member (with voting rights; higher benefits)

- Associate Member (non-voting; same dividends and services access)

Features and Benefits:

- Financial benefits: annual dividends (historically 8%+), patronage refunds, savings and time deposits with up to 3% interest

- Loan programs: for business, agriculture, housing, vehicles, education, medical needs, emergencies, travel, and calamities

- Insurance coverage: life, non-life, loan protection, and health plans

- Convenience services: GCash-enabled ATM card, POS and online payments, fleet card for fuel discounts, member ID with ATM use

- Accessibility: low entry cost (₱440 initial payment), online pre-membership seminars for OFWs, wide branch network

- Other benefits: affordable appliance/phone financing, memorial plans, and water purifier installment program

4. Cebu CFI Community Cooperative

Founded in 1970 in Cebu City, CFI started as a small group of court employees who wanted protection from loan sharks. Over the years, it opened membership to everyone, making it one of the biggest cooperatives in the Philippines with more than 170,000 members nationwide. Today, it offers savings, loans, investments, and health plans while returning profits to members through dividends and refunds.

Target Members:

- Filipino citizens (18 years old and above)

- OFWs who are natural-born Filipinos with residence in the Philippines

Membership types:

- Regular members

- Associate members (non-voting, limited benefits)

Features and Benefits:

- Savings & Deposits: Regular savings, time deposits with tax-free interest

- Investments: Share capital contributions earning annual dividends

- Loans: Salary, business, livelihood, pension, personal, microfinance, and digital wallet loans

- Health Plan (MMAF): Coverage up to ₱100,000 annually, with accredited hospitals nationwide

- Profit Sharing: Dividends, patronage refunds, and tax-free interest on deposits

- Digital Tools: CFI Credit Cash Wallet & virtual credit lines

- Member Rights: Equal voting power, participation in assemblies, access to programs

5. Oro Integrated Cooperative (OIC)

OIC started in 1966 in Cagayan de Oro with only ₱88 capital and has grown into one of the biggest cooperatives in the Philippines, now serving more than 220,000 members. It stands out for its wide branch network, award-winning services, and commitment to improving members’ financial and social well-being. With just ₱3,000 share capital, members gain full ownership, profit-sharing, and access to various financial and social benefits.

Target Members:

- Entrepreneurs

- Employees

- Students

- Farmers

- OFWs, and

- Any Filipino who wants to join

Membership types:

- Regular Member (₱3,000 common share capital)

- Youth Member (ages 7–17, savings-based)

- Associate Member (non-voting, limited benefits)

Features and Benefits:

- Loans: Salary, business, motorcycle, vehicle, housing, agricultural, pension, microfinance, instant, real estate, and providential loans.

- Savings & Deposits: Youth savings, compulsory and dream savings, preferred/time deposits, SAFE Plus (education + insurance), ATM savings with interest.

- Insurance Plans: Life, accident, health, non-life (motor car, fire, calamity, etc.), memorial plans, and education protection insurance.

- Social Benefits: Calamity assistance, cancer patient support, free women’s health screenings.

- Special Programs: Online membership/loan application, fund transfers, online insurance and savings payments.

- Financial Literacy: Wealth-building programs for local and overseas members.

- Income & Profit Sharing: Annual dividends and tax-free interest on share capital.

6. DCCCO Multipurpose Cooperative

DCCCO started in 1968 in Dumaguete City as a small credit cooperative formed to help families struggling with finances and education costs. From only 49 members and ₱1,181.50 in capital, it has grown into one of the country’s top multipurpose cooperatives offering savings, loans, and community services. It offers a wide range of financial products, plus extra benefits like insurance, investments, and even hotel and housing services in exchange for only ₱2,600 total initial cash out requirements (also includes ₱1,000 share capital, savings deposit, membership fee, annual dues, damayan fund, ID, and ATM card fee).

Target Members:

- Any Filipino of legal age living, working, or doing business in DCCCO’s area of operation

- Must attend Pre-Membership Education Seminar/Webinar (PMES/PMEW)

Membership types:

- New Member (less than 6 months)

- Member in Good Standing (MIGS) with tiers: Nickel (6 months), Bronze (2 years), Silver (3 years), Gold (4 years), Platinum (5 years)

- Youth Members (through DCCCO Youth Zone Laboratory Cooperative)

Features and Benefits:

- Savings Products: Emergency Fund, Insurance Fund, RELAX Savings (for leisure), Anniversary Savings, SAYA (retirement), Youth Educational Support

- Loan Products: Salary, Car/Vehicle, Motorcycle, Pension, Hospitalization, Back-to-Back Loan, Revolving Credit Line

- Insurance Coverage

- Investment Opportunities

- Community Programs & Allied Services: DCCCO Hotel, DCCCO Village

- MyPitaka ATM Card: No maintaining balance, accessible via Bancnet

- Membership Benefits: Profit sharing (dividends), financial security, access to credit and savings, training, and community support

7. AFP Finance Center Multi-Purpose Cooperative (AFPFC MPC)

AFPFC MPC was established in 1989 by 109 AFP personnel who pooled their incentives to create a stable financial cooperative. From a small start, it has grown to over ₱8.6 billion in assets and more than 43,600 members nationwide. What makes it stand out is its high dividends, wide loan options, and consistent reputation as one of the country’s top-performing cooperatives.

Target Members:

- Active and retired AFP personnel

- Civilian AFP employees

- Pensioners, legal beneficiaries, and surviving spouses

- Personnel from BuCor, BFP, PVAO, AFPMBAI, OTS, and LGU Montalban

Membership types:

- Regular Members (active/retired personnel and employees)

- Associate Members (pensioners and beneficiaries)

Features and Benefits:

- Dividends: Up to 25% annually (released July & December)

- Patronage Refunds: Profit share every May for loan borrowers

- Savings Products:

- Regular Savings (5% p.a.)

- Special Savings (6–7% p.a. for 360 days/5 years)

- Capital Contribution Account (₱5,000–₱10,000 minimum, with dividends)

- RSA 2 (1.5% p.a. for unclaimed dividends/refunds)

- Loan Products:

- Salary Loan

- Pension Loan

- Back-to-Back Loan / Flexi Loan

- Lump Sum Loan (for retiring personnel)

- Educational, Emergency, Livelihood, Consumption, Economic Development, Short-Term Loans

- Incentives: Loan giveaways (grocery packages, bags, umbrellas), referral bonuses (1.5% of new member’s loan)

- Educational Support: Financial literacy, livelihood, and disaster preparedness seminars

- Other Benefits: Bereavement assistance, loan renewal after 12 payments, loan restructuring for delinquent accounts

8. PLDT Employees Credit and Consumers Cooperative, Inc. (PECCI) Multipurpose Cooperative

PECCI started in 1958 when 15 PLDT employees pooled their resources to help one another with financial needs. From its humble beginnings, it has grown into one of the country’s leading multipurpose cooperatives with thousands of members and strong financial standing. With a focus on savings, loans, and community development, PECCI is best known for its reliable financial services, wide loan choices, and member-focused programs.

Target Members:

- Active or retired employees of PLDT, subsidiaries, and affiliates

- Dependents of members

- Former PECCI members

- Employees of accredited institutional partners

Membership types:

- Regular member

- Associate member

Features and Benefits:

- Affordable short-term, long-term, and special loan products (education, calamity, housing, car, retirement, business, etc.)

- Consumer goods through installment (gadgets, appliances, vehicles, household items)

- Savings and deposit facilities (up to ₱2 million starting June 2025)

- Dividend and patronage refunds based on transactions

- Emergency and calamity loans during disasters

- Free or discounted life insurance coverage for eligible members

- Birthday bonuses and raffle promos

- Exclusive training and financial literacy programs

- Participation in governance and decision-making

- Community programs supporting education, environment, and social development

- Strong customer support and branch services

- Special loan programs (Gender Sensitivity Loan, Back-to-School Loan, Calamity Recovery Loan)

- Travel perks (e.g., free trips for active members through promos)

9. Perpetual Help Community Cooperative (PHCCI)

PHCCI started in 1971 with only 33 members and ₱586 in share capital. Today, it has grown into one of the top cooperatives in the country, with billions in assets and branches across the Visayas. It is known for being a Christ-centered cooperative that helps transform communities through financial services and member-focused programs.

Target Members:

- Filipino citizens, at least 18 years old, who complete the Pre-Membership Education Seminar (PMES).

Membership types:

- Regular Member

- Associate Member

Features and Benefits:

- Savings Accounts: Tax-free interest, ATM savings, junior savings, flexi savings, and business savings.

- Loan Products: Emergency, calamity, instant, grocery, personal, appliance, motorcycle, vehicle, salary, business, and educational loans.

- Dividends & Interest: Earnings from share capital and tax-free interest on savings.

- Scholarships: Financial aid for members’ children or dependents in public or private schools.

- Insurance Assistance: Medical and hospitalization loans.

- Mobile App (GO PHCCI): For easy loan applications, balance tracking, and secure transactions.

- Other Perks: Transparent fees, dedicated staff, extended office hours, and community programs like gift-giving.

10. Sorosoro Ibaba Development Cooperative (SIDC)

SIDC started in 1969 in Sorosoro Ibaba, Batangas, as a small farmers’ group with only 59 members each giving ₱200 to run a community store. Over the years, it expanded to feeds, veterinary supplies, retail, and financial services, officially becoming SIDC in 1997. Today, it is one of the biggest agri-based co-ops in the Philippines, known for affordable loans, savings programs, and strong community support.

Target Members:

- Anyone willing to use SIDC’s services and fulfill member responsibilities.

Membership types:

- Regular member

- Associate member

Features and Benefits:

- Patronage refund (share of yearly profits based on purchases and loans)

- Scholarships and Study-Now-Pay-Later loans

- Emergency loans (up to ₱80,000, fast release)

- Free medical check-ups and medical assistance

- Mortuary and year-end cash incentives

- Technical and marketing support for farmers and entrepreneurs

- Seminars and financial literacy training

- Higher interest on savings and deposits (no tax deducted)

- Access to SIDC retail stores and rebates

- Trip incentives and Christmas gifts for top members

- Tiered loyalty rewards (interest discounts, higher loan limits, fewer requirements)

- Wide loan options: agri loans, business loans, personal loans, housing loans, vehicle loans, appliance loans, solar financing, and more

- Savings products (regular, time deposit, youth savings, future fund)

- Insurance coverage (life, non-life, accident, property, loan protection)

- Agricultural programs (contract growing, feeds dealership, organic fertilizer, training)

- Consumer retail outlets with discounts and patronage perks

- Remittance, bills payment, and e-load services

11. First Isabela Cooperative Bank (FICOBANK)

FICOBANK is one of the pioneer cooperative banks in the country, established in 1976 by local cooperatives to give farmers and small entrepreneurs access to banking services. It started as a small rural bank and is now a multi-branch financial institution with billions in assets and operations in 11 provinces. With a minimum share capital of ₱1,000, members enjoy community-based banking that prioritizes fair and sustainable financial solutions.

Target Members:

- Farmers, fishers, rural and urban workers

- OFWs, professionals, entrepreneurs, students, and the general public

- Foreign nationals (with valid requirements)

- Registered cooperatives (agri, marketing, multi-purpose, credit, and Samahang Nayon)

Membership types:

- Individual Client-Member

- Institutional Member (cooperatives)

Features and Benefits:

- Deposit Products: Savings, time deposits, checking, kids’ savings, high-interest savings, and special accounts

- Loans: Agri loans, MSME loans, commercial loans, multi-purpose loans, vehicle/machinery loans, jewelry loan, and OFW/enterprise loans

- Other Services: Bills payment, money transfers, remittances (Western Union/GCash), interbranch deposits, digital rural banking, microinsurance

- Earnings: High interest rates (2–5% per year on some savings), quarterly compounded interest, dividends from share capital

- Benefits: Wide branch network, BSP-recognized top cooperative bank, award-winning service, and member-driven governance

12. Bureau of Jail Management and Penology Multipurpose Cooperative (BJMP MPC)

BJMP MPC was formed to provide financial assistance and savings opportunities for personnel of the Bureau of Jail Management and Penology (BJMP) and their families. With only ₱200 initial share capital and a ₱50 membership fee, members can enjoy affordable loans, savings programs, and cooperative benefits. It is known for its transparency, fast loan approval, and community-focused services, making it a reliable partner in financial growth.

Target Members:

- BJMP employees and uniformed personnel

- Regular staff assigned to BJMP offices

- Family members or dependents (as associate members, subject to approval)

Membership types:

- Regular Member

- Associate Member

Features and Benefits:

- Salary, emergency, educational, calamity, housing, car, and multi-purpose loans

- Low interest rates (e.g., calamity loans)

- Quick loan approval and salary deduction payment option

- Savings growth through share capital contributions

- Patronage refunds and interest on share capital

- Ownership stake with voting rights (for regular members)

- Free seminars, training, and community programs

- Financial support during life events (schooling, housing, emergencies, calamities)

- Access to a stable, service-driven cooperative

13. Providers Multipurpose Cooperative (PMPC)

PMPC started in 2008 as a small savings and credit group of 24 COA employees in Isabela with only ₱12,000 pooled capital. It has since grown into a multipurpose cooperative recognized by the Cooperative Development Authority, with an authorized share capital of ₱4 million and over 27,000 members across Luzon. PMPC is known for its wide range of financial services, strong member support programs, and opportunities to grow through loans, investments, and community benefits.

Target Members:

- Filipino citizens, 18 years old and above, employed or self-employed, and residing in Luzon.

Membership types:

- Regular Member (with voting rights and full privileges)

- Associate Member (with access to services but no voting rights)

Features and Benefits:

- Loans: Salary, bonus, pension, honorarium, livelihood, agriculture, real estate, car/motorcycle, and business loans.

- Deposit Services: Time deposit options for individuals and businesses.

- Healthcare Services: Providers Medical Center offering pediatrics, cardiology, surgery, laboratory, and pharmacy services.

- Memorial Services: Cremation, funeral packages, memorial garden, and funeral investment plans.

- Consumer Goods & Services: Access to appliances, gadgets, automobiles, internet subscription (iProviders), and Providers Food & Nuts.

- Member Benefits: Interest earnings on share capital, patronage refunds, Damayan assistance (financial help during emergencies), access to cooperative programs, and participation in training and assemblies.

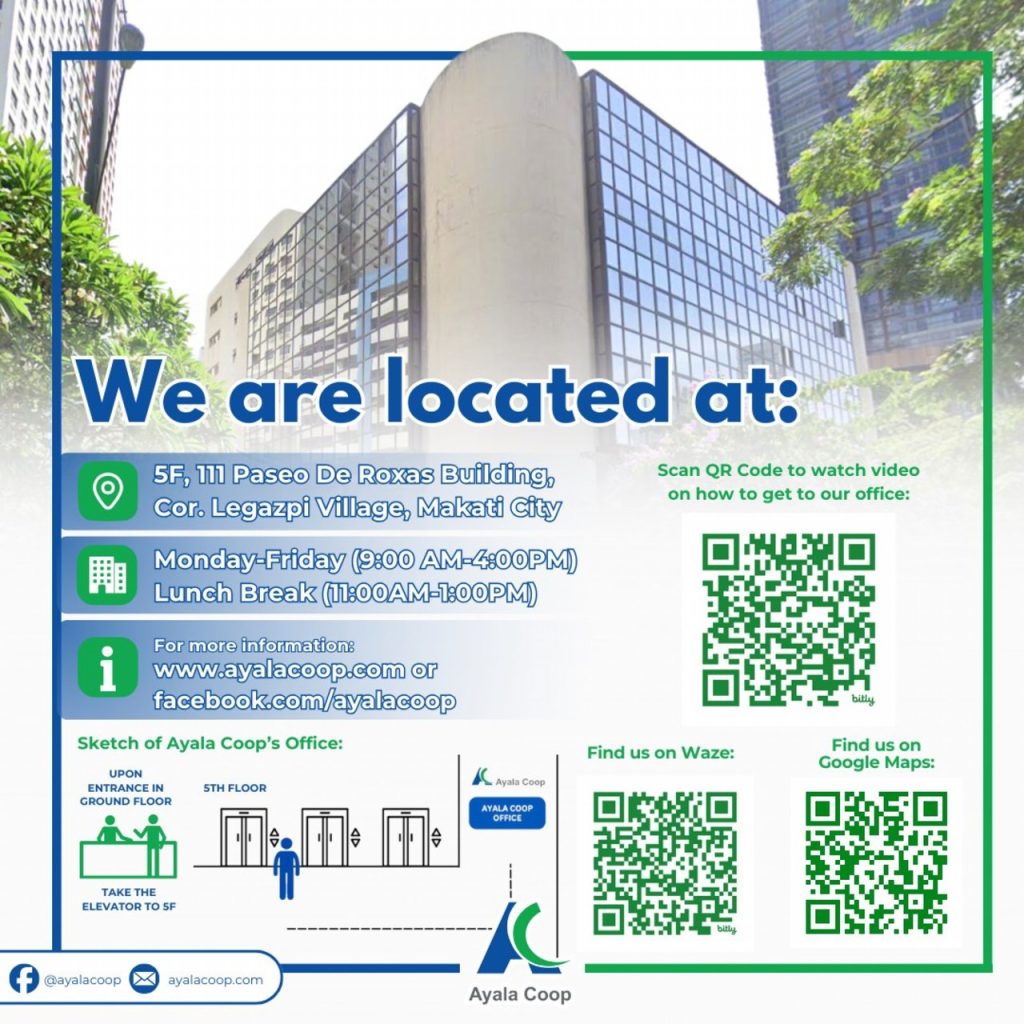

14. Ayala Multi-Purpose Cooperative (AMPC)

Founded in 1995 by 21 Ayala employees with only ₱10,500 in capital, AMPC has grown into one of the country’s top institution-based cooperatives, now worth over ₱2 billion. It serves as a financial partner for Ayala Group employees through savings, loans, and tax-free dividends. The cooperative is best known for its wide loan options, long-term savings programs, and exclusive benefits for members.

Target Members:

- Employees of Ayala companies with at least 20% Ayala ownership.

Membership types:

- Regular Member: Regular or permanent Ayala employees

- Associate Member: Retired or resigned members with good credit standing

- Associate Project Member: Project-based employees with at least 1 year of service and 8 months remaining in contract

Features and Benefits:

- Tax-free dividends on share capital

- Patronage refunds based on loan interest paid

- Wide range of loan products (auto, housing, education, emergency, travel, wedding, multipurpose, etc.)

- Flexible loan amounts depending on share capital

- Long-term savings through regular share capital build-up (min. ₱100 per payday)

- Refundable share capital upon membership termination (after clearing loans)

- Continued membership after resignation/retirement (with good standing)

- Exclusive perks and tie-ups with Ayala companies and partners

- Stock certificates for every ₱50,000 share capital contribution

- Participation rights in General Assembly and cooperative decision-making

- Customer support services and assistance for members and beneficiaries

15. Gubat St. Anthony Cooperative (GSAC)

Founded in 1964 in Gubat, Sorsogon, GSAC began as a small parish-based credit union with only ₱222 in funds. Today, it is one of the biggest cooperatives in Bicol with over 60,000 members, billions in assets, and branches across Sorsogon, Albay, Camarines Sur, and Northern Samar. Known for its wide range of financial, health, retail, and agricultural services, GSAC continues to grow while giving back to its members and community.

Target Members:

- Anyone 18 years old and above

- Must have a source of income

Membership types:

- Regular Member

- Associate Member

- Laboratory Cooperative Member (for youth)

Features and Benefits:

- Access to savings and time deposit programs (education, retirement, children’s savings)

- Wide range of loans (personal, salary, housing, business, OFW, agricultural, medical, appliance, car, pension, SME, etc.)

- Dividends and patronage refunds

- Loyalty awards and pension programs

- Damayan II death aid assistance

- Insurance packages (personal, family, vehicle, fire, surety bonds)

- Discounts and reward points at GSAC-owned businesses (mart, pharmacy, hotel, etc.)

- Access to GSAC General Hospital and agri-industrial services

- Free trainings, seminars, and financial literacy programs

- Participation in decision-making with voting rights

- Community support and marketing assistance for businesses

16. Benguet Electric Cooperative (BENECO)

BENECO was founded in 1973 to bring electricity to Baguio City and Benguet Province and was granted a 50-year franchise in 1978. From only serving a few areas, it reached 100% barangay electrification by 2012, making it one of the top-performing electric co-ops in the Philippines. With billions in assets and over 143,000 members, BENECO is known for reliable power service, transparency, and community-focused programs.

Target Members:

- Property owners in Baguio and Benguet

- Tenants with authorization from property owners

- Residential, commercial, and temporary connection applicants

- New members who attend the Pre-Membership Education Seminar (PMES)

Membership types:

- Individual membership

- Joint membership (husband and wife)

Features and Benefits:

- Reliable and affordable electricity supply across Baguio and Benguet

- Renewable power generation projects (mini-hydro plants)

- Broadband and communication services

- Access to income-generating ventures and rental opportunities

- Rural electrification support for remote communities

- Member education programs (PMES and training)

- Participation in a democratic, member-owned organization

- Membership perks for only ₱100 (plus ID fee ₱42)

- Community development initiatives that improve livelihoods and services

17. Sacred Heart Savings Cooperative (SHSC)

SHSC started in 1972 in Galimuyod, Ilocos Sur with just 33 parishioner-members and ₱916 share capital. From a small credit union, it has grown into a leading multipurpose cooperative with over 60,000 members and 20+ branches across Northern and Central Luzon. With an affordable ₱1,500 capital requirements and a wide range of financial and community services, SHSC is one of the best options for Filipinos looking for both savings growth and social support.

Target Members:

- Adults (18 years old and above)

- Children/Youth (1–17 years old, through Laboratory Coop)

- Farmers, small entrepreneurs, professionals, OFWs, drivers, and residents near SHSC branches

Membership types:

- Regular Membership (Adults 18+)

- Laboratory Cooperative Membership (Children and Youth)

Features and Benefits:

- Wide variety of loan products (business, agriculture, multipurpose, car loans, microfinance)

- Savings programs (regular, time deposit, retirement, goal savings, birthday savings)

- Dividends from share capital contributions

- Patronage refunds based on services used

- Retirement savings with 5% annual interest

- Birthday savings converted into a birthday cake reward

- Health care and community benefits via the Saranay Program

- Access to coop-run businesses (clinic, grocery, bazaar, resort, printing services)

- Gifts, incentives, and special rewards for members

- Voting rights and ability to run for cooperative office

- Participation in assemblies and decision-making

- Stable and award-winning cooperative with strong community presence

18. Tam-an Banaue Multipurpose Cooperative (Tam-an BMPC)

Founded in 1991 with only 25 members and ₱25,000 in assets, Tam-an BMPC has grown into a multi-billion-peso cooperative with over 200,000 members and dozens of branches across Luzon. It started as a hog raisers’ group in Banaue, Ifugao, initiated by Jose D. Tomas, Sr., and eventually expanded into finance, tourism, construction, and more. Today, it is one of the country’s top co-ops, offering strong financial returns, community programs, and diverse business ventures.

Target Members:

- Individuals 18–65 years old

- Open to all, regardless of profession or location

Membership types:

- Regular Member

- Associate Member

Features and Benefits:

- Loan Products: Regular, business, market vendor, housing, agricultural, vehicle, emergency, rice, bayanihan, P3 loan, techno loan, and more (up to ₱50M).

- Savings & Deposits: Regular savings (2%/year), time deposit (5%/year), Pangarap savings (4%/year), share capital dividends.

- Member Benefits:

- Hospitalization and lifetime health coverage

- Damayan benefit (up to ₱150,000 in case of death)

- Accident hospitalization and death benefits (up to ₱200,000)

- Business Ventures: Hotel and resort, gasoline stations, TESDA-accredited training center, eco-tourism farm, construction and agri-supply outlets, event spaces, commercial stalls.

- Social Programs: Scholarships, blood donation program, free medical check-ups, door-to-door collection, barangay and school support, senior citizen benefits, community events, financial literacy training, and field trips for members.

- Other Perks: Competitive loan and deposit rates, fast loan processing, business opportunities, discounts, and lifetime healthcare.

19. Novaliches Development Cooperative (NOVADECI)

Founded in 1976 by 15 market vendors with just ₱7,000 pooled capital, NOVADECI has grown into one of the largest multipurpose cooperatives in Luzon. It offers financial, medical, livelihood, and social services while promoting transparency and member empowerment. With over 40 years of service, it stands out for affordable credit, health programs, and strong community support—making it a great choice for individuals seeking stability and inclusive growth.

Target Members:

- Employees, entrepreneurs, self-employed, and individuals engaged in livelihood activities (18–60 years old, living or working in Luzon).

Membership types:

- Regular Membership

- Associate Membership

Features and Benefits:

- Loans: Business, educational, emergency, housing, utility, commodity, rice, Christmas, memorial plans, and more.

- Savings & Investments: Share capital, time deposit, preferred shares, and special savings (education, housing, prime).

- Medical Services: NOVADECI Health Care Program (NHCP), consultations, lab tests, pharmacy, therapy, and medical missions.

- Social Programs: Scholarships, livelihood support, housing projects, COOP-AKSI, Damayan, Tangkilikan, and SSS partnership.

- Insurance & Protection: NMSB benefits (death, disability, retirement, partial advances).

- Member Perks: Dividends, rebates, discounts from partner schools/businesses, grocery & rice products, online store, and convention rentals.

- Community & Governance: Participation in assemblies/elections, training & seminars, transparent operations, and outreach activities.

20. Panabo Multipurpose Cooperative (PMPC)

PMPC began in 1963 as a small parish-based credit union in Panabo, Davao del Norte with only ₱130 capital and has grown into one of the leading cooperatives in Mindanao with billions in assets. It requires a minimum of ₱2,000 share capital (8 shares at ₱250 each) to join. Members trust PMPC because it offers safe, transparent, and sustainable financial services with international standards.

Target Members:

- All Filipinos 18 years old and above who attend the Pre-Membership Education Seminar (PMES) and subscribe to the required share capital.

Membership types:

- MIGS-GOLD (with voting rights, can run for election)

- MIGS-SILVER (discussion rights, no voting)

- MIGS-BRONZE (attendance only)

- NON-MIGS (not eligible for assemblies)

Features and Benefits:

- Savings Options: Regular Savings, Youth & Teen Savers, Golden Savers (senior citizens), Aflatoun School Savings, Time Deposits, ATM services

- Loans: Business, personal, emergency, consumer, pension, lot purchase, special loans (flexible terms, low interest)

- Insurance & Protection: Life and non-life insurance, accident insurance (up to ₱50,000), CTPL, fire, student accident insurance, mortuary assistance

- Member Benefits: Annual dividends, patronage refund, free accident insurance, scholarship program, transformation and training programs

- Special Programs: Women entrepreneurship support, affordable housing projects, youth and education initiatives (scholarships, Adopt-a-Classroom, Brigada Eskwela, school tours, youth camps)

21. Lamac Multipurpose Cooperative (LMPC)

Founded in 1973 in Lamac, Pinamungajan, Cebu, LMPC started with just 70 farmers contributing ₱50 each, pooling a total of ₱3,500. From solving basic community needs like roads and water, it grew into one of the biggest and most awarded cooperatives in the country, with more than 150,000 members across Visayas and Mindanao. Today, LMPC is known for its diverse services—ranging from loans and livelihood support to tourism, agribusiness, and community development.

Target Members:

- Residents of Visayas and Mindanao, farmers, micro-entrepreneurs, workers, professionals, and community members seeking livelihood or financial support.

Membership types:

- Regular Member

- Associate Member

Features and Benefits:

- Financial Services & Loans:

- Group lending (HELP)

- Micro-entrepreneur loans (ME)

- Small & medium business loans (SMILE)

- Larger loans for excellent members (RELAX)

- Agricultural loans (KOMBATI), emergency loans, pension loans, salary loans, provident loans

- Community Enterprises:

- Coop Mart, bakery, water refilling station, pasalubong center

- Gasoline station, garments shop, dairy box (Cebu), Coca-Cola bottling facility

- Tourism & Hospitality:

- Hidden Valley Mountain Resort & Wavepool

- Hidden Valley Beach Resort

- Bugsay Resto Grill, Cocoville Resort

- Organic farm & resort experiences

- Agri-Business & Processing:

- Dairy processing plant, tablea processing, coco sugar processing, dairy soap making

- Education & Training:

- Integrated Organic Farm School (TESDA-accredited)

- Courses in organic farming, entrepreneurship, and livelihood skills

- Farm tourism activities (vermicomposting, livestock handling, organic inputs)

- Community Benefits:

- Employment opportunities in coop-run businesses

- Education and training programs

- Infrastructure and livelihood projects in member communities

22. PERA Multipurpose Cooperative (PERA MPC)

Founded in 1998 by 29 Philippine National Bank employees, PERA MPC started small but has grown into one of the biggest financial cooperatives in the country with over 16,000 members and billions in assets. With a minimum share capital requirement, it gives Filipinos access to affordable financial services like savings, loans, and investments. It’s best known for flexible loan options, high time deposit rates, and its commitment to community development, making it a great choice for workers, pensioners, OFW families, and small entrepreneurs.

Target Members:

- Employees

- Entrepreneurs

- OFW families

- Pensioners

- Farmers

- Traders

- Vendors

- IPs and

- Local community members

Membership types:

- Regular Member

- Associate Member

Features and Benefits:

- Loans: Regular, emergency, pension, capitalization, hold-out, and flexible capital loans with competitive terms.

- Savings & Deposits: Time deposits with interest up to 8% annually (minimum ₱10,000).

- Loan Insurance Coverage: Protection for borrowers.

- Fuel Services: Gusty Shone gasoline stations with Seventeen Best Bai convenience stores.

- Café: KaPERA Brew, serving local coffee blends.

- Community Programs: Financial aid and livelihood support for disaster-hit areas and Indigenous Peoples.

- Income Potential: Dividends and patronage refunds from cooperative surplus.

23. Benguet State University and Community Multipurpose Cooperative (BSUCMPC)

BSUCMPC started in 1984 as a teachers’ and employees’ cooperative and grew into one of the biggest and most trusted co-ops in the Cordillera Region. With a minimum share capital of ₱20,000 (payable in 3 years), it has reached “Billionaire Cooperative” status due to its strong financial performance. Members benefit from affordable loans, savings and investment programs, and community-centered services—making it ideal for anyone who wants both financial growth and social support.

Target Members:

- BSU employees and staff

- Residents of the Cordillera and nearby provinces

- Government and private workers

- Farmers, entrepreneurs, OFWs, retirees, students, and youth

Membership types:

- Regular Member

- Associate Member

- Laboratory Member (0–23 years old)

- Re-entry Member

Features and Benefits:

- Investments & Savings: Share capital, savings deposits, time deposits, long-term deposits, kiddie savings, ATM services, bills payment, remittance, insurance

- Loans: Business, agricultural, housing, calamity, emergency, salary-deduction, appliance, grocery, travel, shopping, and more

- Financial & Social Support: Mutual aid fund, hospitalization assistance, funeral aid, scholarship grants, medical missions, environmental programs

- Other Services: Apartment and boarding rentals, commercial spaces, POS/ATM services, seminars, and continuous member education

24. Solidaritas Credit Cooperative (SCC)

SCC is a church-based cooperative established in 1992 by priests from the Archdiocese of Manila, originally known as Bahay-Pari Credit Cooperative. It requires a minimum share capital of ₱10,000 and is exclusive to Catholic clergy, offering savings, investments, and loan services tailored to their needs. With its faith-centered foundation, SCC is ideal for clergy who want both financial stability and a supportive spiritual community.

Target Members:

- Catholic bishops, priests, and deacons in the Philippines

Membership types:

- Regular membership (exclusive to clergy)

Features and Benefits:

- Savings accounts (earn interest with at least ₱100,000 balance)

- Loan products exclusive for clergy

- Investment opportunities within the cooperative

- Climbs Insurance coverage

- Share capital may serve as collateral for loans

- Access to democratic, faith-based cooperative governance

- Long-term financial planning support aligned with priestly life

- Participation in programs promoting social responsibility and solidarity

25. Sta. Cruz Savings and Development Cooperative (SACDECO)

Founded in 1982 and formally established in 1984, SACDECO started as a small credit cooperative with only 25 incorporators and ₱5,000 capital. Over the years, it has expanded to serve individuals, families, and communities across Sta. Cruz, Ilocos Sur and beyond. With affordable share capital requirements (amounting to ₱3,000 share capital + other fees (₱8,750 total for ages 18–65) and ₱5,000 share capital + other fees (₱10,750 total for ages 66 and above)), SACDECO is known for its wide range of savings, loans, and insurance services that make it one of the most trusted co-ops in the country.

Target Members:

- Residents of Sta. Cruz, Ilocos Sur and nearby towns

- Farmers, fisherfolk, and micro-entrepreneurs

- Tricycle drivers/operators, OFWs, mothers, and single parents

- Students, youth, salaried employees, professionals, retirees, and senior citizens

Membership types:

- Regular Members (18–65 years old)

- Senior Members (66 years old and above)

- Youth/Student Members (via Laboratory Cooperative programs)

Features and Benefits:

- Savings Programs: Regular, time, retirement, emergency, mother savings, youth/teen savers, OFW cash builder, and health savings plans

- Loan Programs: Personal, business, agricultural, real estate, green finance, recovery loans (Bangon, SAGIP, KOMTEK, ANYO)

- Insurance & Protection: Loan protection, accident, death, and health insurance (SAI, MEDICAIDE, etc.)

- Convenience Services: Bills payment via SM and Bayad Centers, ATM access

- Special Programs: Financial literacy seminars, cooperative advocacy, student/youth programs, community and environmental initiatives

- Community Benefits: Old age welfare, marital benefits, feeding programs, medical missions, sanitation projects

- Financial Returns: Dividends and patronage refunds based on share capital and transactions

- Other Perks: Function hall use for events, ownership and voting rights in the coop

Video: Top Cooperatives in the Philippines

Now that we’ve rounded up some of the top cooperatives in the country, here’s a video you can watch to learn more about how these top cooperatives work and how it can help you build a more stable financial future for yourself and your family:

Need More Help?

For any questions, complaints or anything related to cooperatives, you may reach out to:

Cooperatives Development Authority

- Main Office Address: 827 Aurora Blvd., Service Road, Brgy. Immaculate Conception Cubao, 1111 Quezon City, Philippines

- Email Address: helpdesk@cda.gov.ph

- Contact Number: (02) 8725-3764

- Website: www.cda.gov.ph

- Facebook: https://web.facebook.com/CDAphgov?_rdc=1&_rdr

- Youtube: https://www.youtube.com/c/CDAPhilippinesgov